Akbank T.A.Ş. Corporate Policy

Purpose of Akbank T.A.Ş. Corporate Policy is to ensure compliance with Turkish and international regulations regarding financial crimes and assuring compliance with obligations associated with prevention of laundering proceeds of crime, financing of terrorism and proliferation of weapons of mass destruction. The Policy is prepared in line with Akbank Financial Group Corporate Policy,

Legal and Regulatory Framework in Türkiye

The abuse of the financial system to launder money resulting from crimes is a criminal offence in Türkiye. Fight against laundering proceeds of crime and combatting of financing of terrorism is conducted by Financial Crimes Investigation Board (MASAK), which is a main service unit of Ministry of Finance.

The principal requirements, obligations and penalties can be found in:

International Legislation

The structures of Akbank T.A.S.'s AML/ KYC Standards policy are:

- Complying with AML (Anti- Money Laundering) and CFT (Combating Financing of Terrorism) laws and regulations such as; local laws (Turkish AML Act and Criminal Act) and regulatory guidance, U.N. Security Council Resolutions, EU Directives, USA Patriot Act.

- Recommendations made by the FATF (Financial Action Task Force) Standards on AML and CFT standarts and Application Methodology Criteria, NCCT Reports.

- Evaluating KYC (Know Your Customer) principles and customer identification regulations such as; Basel Principles (Customer due Diligence for Banks), Wofsberg Principles, TBA Local Industry Guidance/ Best Practices.

AML/CFT/ CPF Program and Applications

Akbank T.A.S instituted appropriate procedures for controlling activities to comply with all applicable laws and regulation in Türkiye and international standards for the need to have adequate systems and controls in place to mitigate the risk of the firm being used to facilitate financial crime. Akbank T.A.S.'s AML/CFT/CPF Program includes;

- A designated AML Compliance Officer and Compliance Unit,

- Written policies, procedures and guidelines,

- Risk based controls, including AML software program that monitors ongoing transactions, account activites of customers and screens existing and prospective customers for AML, CFT and CPF purposes,

- Procedures for reporting suspicious activity internally and to relevant law enforcement authority,

- Record keeping according to local laws,

- Training,

- The internal audit operations and independent audit testing.

Sanctions Policy

Akbank is committed to compliance with relevant economic and trade sanctions laws in all jurisdictions in which it operates through identifying, mitigating and managing the risk. Policy applies to all countries and/or jurisdictions in which Akbank operates and extends to any additional countries and/or jurisdictions where Akbank commences operations and/or has an active registration or license.

All Akbank Group domestic and international, branches and subsidiaries must to comply with all applicable sanctions laws and regulations published by below authorities. United Nations, US Office of Foreign Assets Control (OFAC), European Union, United Kingdom Treasury (UK HMT), etc.

All employees receive training on International Sanctions Regulations annually. Related training given by Akbank’s compliance team.

All Policy incidents and breaches must be reported to the Group Compliance Officer.

Customer Acceptance Policy

The Bank’s risk based methodology is reflected on the Customer Acceptance Policy. Policy includes principles that ensure compliance with the "Know Your Customer" principle. The obligation to know customers begins with the identity verification step.

According to the Bank’s policy, the persons and entities non-eligible for acceptance as a customer are as listed below:

- Those who refuse to provide the necessary information and documents for identity verification and customer identification, and who avoid registration;

- Customers who have received negative opinions as a result of controls conducted for customer groups considered high-risk, for whom stricter measures are applied for customer acceptance in line with the risk-oriented principle;

- Those who wish to open accounts with anonymous/pseudonym/fictitious names or without an identity;

- Those who do not provide convincing/sufficient information about their transactions and the source of their funds;

- Those whose names appear on lists published by national and international institutions and organizations that include those involved in money laundering, financing of terrorism, and supporting the proliferation of weapons of mass destruction;

- Those who have a problematic record in our bank's internal intelligence system regarding money laundering, financing of terrorism, proliferation of weapons of mass destruction, and related financial crimes;

- Shell banks;

- Natural and legal persons residing in countries under sanctions;

- Persons whose names appear on Asset Freezing Decisions/Lists.

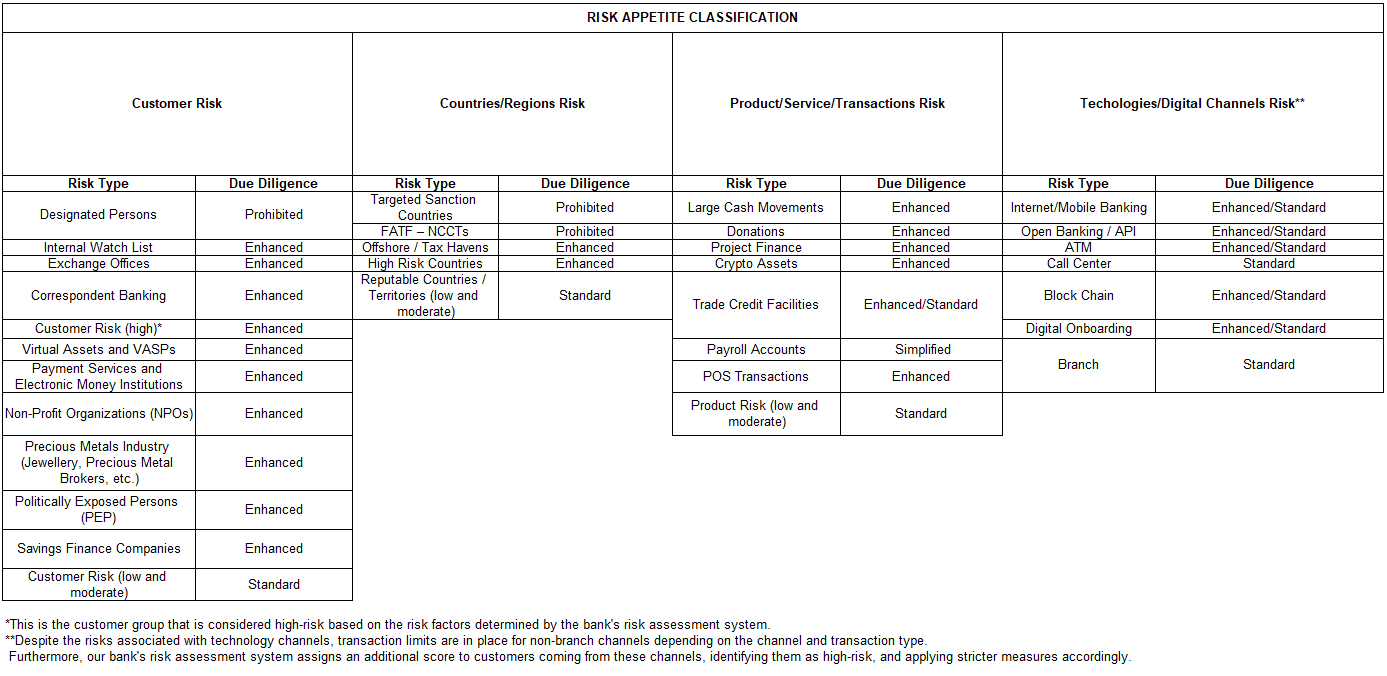

The Bank acts in accordance with the risk factors and types defined in the Corporate Policies. Risk perception is updated with a proactive methodology based on a risk based approach. The four basic elements that constitute our bank's risk perception are given below, and risk appetite is defined in line with these four risk elements.

- Customer Risk

- Product/Service/Transaction Risk

- Geographic/Country Risk

- Technology/Channel Risk

Bank's risk appetite is determined according to the risk assessment that is regularly carried out in all areas related to compliance with legal regulations, money laundering, financing of terrorism, financing of the proliferation of weapons of mass destruction, sanctions and financial crime risks, and is reviewed periodically by the Board of Directors within the scope of the Corporate Policy. Our bank's risk appetite classification table is given below.

High Risk Customers

High risk customers are customer groups that are considered riskier than others due to the nature of their transactions, their legal status, or their financial structure. Certain kinds of businesses may require EDD at account opening. Below are customers whose risk level is considered relatively high:

- Exchange Offices, Jewelers, Precious Stone and Metal Traders,

- Foreign Trade (transit trade companies),

- Transportation/Shipping,

- Customs Brokerage Activities (Customs Offices),

- Automotive Spare Parts Manufacturing and Trading,

- Factoring Companies, Electronics and IT Companies, Consulting Firms,

- Cash-Intensive Business Sectors (parking lots, restaurants, fuel, beverage, tobacco companies, etc.),

- Defense and Weapons Industry,

- Non-Profit Organizations,

- Gambling,

- Savings Finance Companies,

- Electronic Money and Payment Institutions,

- Crypto Asset Service Providers.

High Risk Services, Products and Transactions

The following services, products, and transactions are identified as high-risk:

- Transactions affected with high risk countries,

- Foreign money transfers of high amounts,

- Cash depositing transactions in high amounts,

- Complicated and extraordinary transactions,

- Products and services which are not consistent with the customer’s profession or fields of activity, risk profile and fund sources,

- Services which may become exposed to fraud due to newly introduced products and technologic developments,

- Transactions executed by using systems allowing non-face-to-face transactions.

- Correspondent Banks

High Risk Countries and Regions

Geographic risk assessment of risky countries and regions is based on the following definitions, criteria, and lists published by national/international institutions/organizations:

- Tax havens (according to FATF criteria),

- Countries subject to a full or partial embargo by European Union (EU),

- Countries subject to a full or partial embargo by United Nations,

- Countries subject to a full or partial embargo by United Kingdom Treasury (UK HMT),

- Countries subject to a full or partial embargo by OFAC (United States, Department of Treasury),

- Countries and regions included in the list of countries and regions which do not enter into cooperation with FATF (Financial Action Task Force),

- Countries named in FINCEN (United States, Financial Crimes Enforcement Network) list.

Training

To ensure compliance with the obligations imposed on banks under the laws and related regulations concerning the prevention of money laundering, financing of terrorism, and financing of the proliferation of weapons of mass destruction, training activities are conducted to increase the knowledge and awareness level of our bank personnel. These training activities are supported by best practice examples that explain the basic principles of Turkish and international legislation. The planning and coordination of training activities are carried out under the supervision of the Compliance Officer, in coordination with Akbank Academy, through risk-focused customized trainings within the annual training program.

AML Questionnaire

For Anti-Money Laundering Quesitonnaire form, please click here!

Patriot Act Certification

Please click here for certification regarding correspondent accounts for foreign banks.